Multivariate Generalized Autoregressive Conditional Heteroskedasticity (MGARCH) models

dsem can be specified to estimate variation over time in

a parameter representing the magnitude of exogenous variance (i.e.,

two-headed arrow). This essentially allows dsem to function

as a Multivariate Generalized Autoregressive Conditional

Heteroskedasticity (MGARCH) model, while allowing missing values for

covariates that drive changes in variance.

To show this, we simulate three time-series of length, with no correlation but a steady increase in the standard deviation over time:

Exploratory MGARCH

We first fit this without any covariate. To do so, we specify a

latent variable F that follows a random walk with unit

variance. This variable the moderates the double-headed arrows

(representing the magnitude of exogenous variance) for each

time-series:

# Define data including latent factor for heteroskedasticity

dat = data.frame(

setNames( data.frame(eps_tc),letters[seq_len(n_vars)]),

F = NA

)

# Define SEM using F as latent moderating variable

sem = "

a <-> a, 0, F

b <-> b, 0, F

c <-> c, 0, F

F <-> F, 0, sdF, 0.1

F -> F, 1, NA, 1

"

# exploratory fit

fit1 = dsem(

tsdata = ts(dat),

sem = sem,

estimate_mu = colnames(dat),

control = dsem_control(

use_REML = FALSE,

gmrf_parameterization = "full",

logscale_moderating_variance = TRUE,

quiet = TRUE

)

)

# Inspect estimates

summary(fit1)

#> path lag name start parameter first second direction Estimate Std_Error

#> 1 a <-> a 0 F NA 0 a a 4 NA NA

#> 2 b <-> b 0 F NA 0 b b 4 NA NA

#> 3 c <-> c 0 F NA 0 c c 4 NA NA

#> 4 F <-> F 0 sdF 0.1 1 F F 2 0.07221498 0.0252122

#> 5 F -> F 1 <NA> 1.0 0 F F 1 1.00000000 NA

#> z_value p_value

#> 1 NA NA

#> 2 NA NA

#> 3 NA NA

#> 4 2.864287 0.004179491

#> 5 NA NAThe model has a nonzero estimate of sdF representing the

variance over time in heteroskedasticity (in log-space), suggesting that

the model detects the heteroskedasticity.

Confirmatory MGARCH

Alternatively, we might specify a covariate that is hypothesized to drive heteroskedasticity. In this case, we simply specify a trend over time as covariate, and estimate its impact on the latent moderating variable. To avoid confounding between the random-walk for the latent variable and the trend covariate, we also remove the random-walk from the latent factor. Finally, we randomly simulate missing data in the covariate, to show that the MGARCH can still accomodate data that are missing at random:

# Define data including latent factor for heteroskedasticity and covariate

dat = data.frame(

setNames( data.frame(eps_tc),letters[seq_len(n_vars)]),

F = NA,

slope = scale( seq_len(n_times), center = TRUE, scale = TRUE )

)

# Randomly simulate 10% missing data for covariate

dat$slope[ sample(seq_len(n_times), n_times/2) ] = NA

# Define SEM using F as latent moderating variable

# and slope as covariate for F

sem = "

a <-> a, 0, F

b <-> b, 0, F

c <-> c, 0, F

F <-> F, 0, sdF, 0.1

slope <-> slope, 0, sd_slope

slope -> slope, 1, NA, 1

slope -> F, 0, beta

"

# confirmatory MGARCH

fit2 = dsem(

tsdata = ts(dat),

sem = sem,

estimate_mu = colnames(dat),

control = dsem_control(

use_REML = FALSE,

gmrf_parameterization = "full",

logscale_moderating_variance = TRUE,

quiet = TRUE

)

)

# Inspect estimates

summary(fit2)

#> path lag name start parameter first second direction

#> 1 a <-> a 0 F NA 0 a a 4

#> 2 b <-> b 0 F NA 0 b b 4

#> 3 c <-> c 0 F NA 0 c c 4

#> 4 F <-> F 0 sdF 0.1 1 F F 2

#> 5 slope <-> slope 0 sd_slope NA 2 slope slope 2

#> 6 slope -> slope 1 <NA> 1.0 0 slope slope 1

#> 7 slope -> F 0 beta NA 3 slope F 1

#> Estimate Std_Error z_value p_value

#> 1 NA NA NA NA

#> 2 NA NA NA NA

#> 3 NA NA NA NA

#> 4 0.10617048 0.112550326 0.9433156 3.455195e-01

#> 5 -0.04800428 0.004794621 -10.0121119 1.348428e-23

#> 6 1.00000000 NA NA NA

#> 7 0.32588875 0.046440238 7.0173790 2.260688e-12The model has a positive estimate of beta, indicating

that it attributes some portion of heteroskedasticity to the

hypothesized covariate.

Comparison

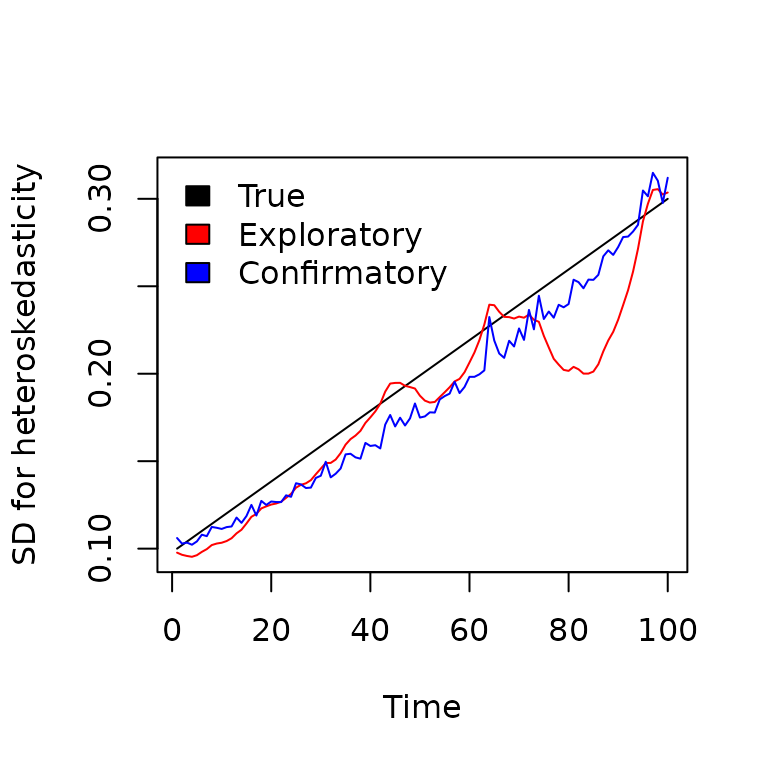

We can then plot these estimated variances against the true (simulated) value

# Bundle true and estimated time-series

Y = cbind(

True = sigF_t,

exp(predict(fit1)[,4]),

exp(predict(fit2)[,4])

)

#

matplot(

x = seq_len(n_times), y = Y, type = "l", lty = "solid",

col = c("black","red","blue"), xlab = "Time",

ylab = "SD for heteroskedasticity"

)

legend( "topleft", fill = c("black","red","blue"), bty = "n",

legend = c("True", "Exploratory", "Confirmatory"))

As expected, using a covariate improves the estimated heteroskedasticity even in the presence of missing data.

Runtime for this vignette: 3.67 secs